Hyperscale Bonanza

State of the Union:

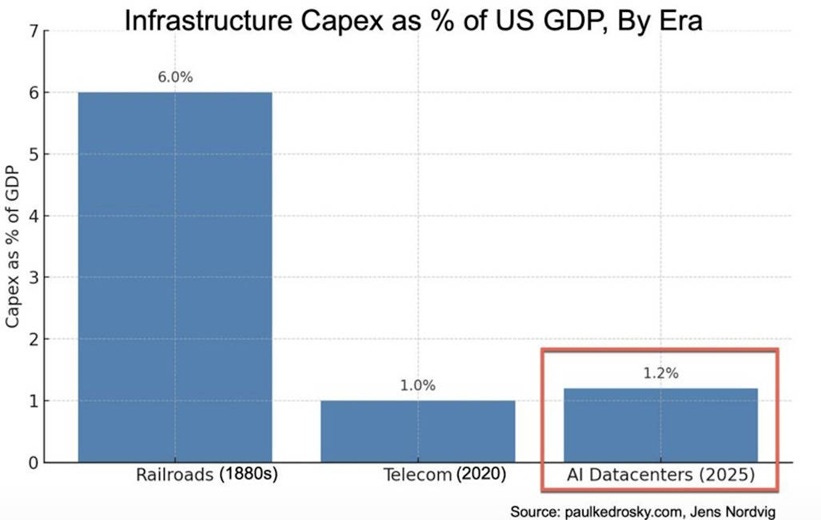

As of August 2025, AI-related investment has contributed more to economic growth than all the growth in consumer spending combined. As a % of GDP it has already surpassed the telecom boom of the 2010s.

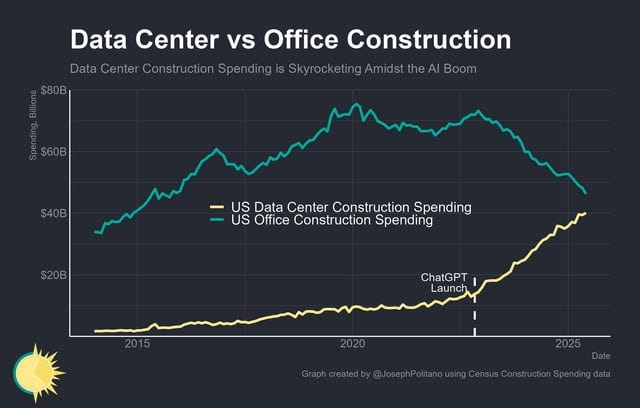

From a construction standpoint, data centers drove > 70 % of the year-over-year rise in private U.S. non-residential construction spending as of March 2025. As a category, Data Center construction is nearing the total of US office construction spend; this would have been unthinkable even just 5 years ago.

When considering the global stage, the United States accounts for roughly 40% data center capacity of global infrastructure, hosting over 5,300 data centers in 2024.

Across the U.S. markets like Virginia, Dallas, Phoenix, and Silicon Valley have all become hot beds for data center construction.

Data Center Origins

Wave One: The Computer - Mainframe computer rooms of the 1940s–1960s, such as the ENIAC required specialized environments for cooling and cabling.

Wave Two: IT - In the 1980s, as businesses deployed more IT equipment and consolidated servers into dedicated rooms.

Wave Three: The Internet - The late-1990s dotcom boom then fueled a surge in data center construction, with many firms building large internet data centers (IDCs) to host websites and online services, featuring redundancies for nonstop operation.

Wave Four: Cloud - In the 2010s, data center growth accelerated globally as companies moved from on prem-server hosting to cloud providers.

Wave Five: AI - Hyperscale campuses rise in the 2020’s. Mega-projects are underway to feed the insatiable compute demands of artificial intelligence.

Data Center Types:

Enterprise: Privately owned facilities dedicated to a single organization’s IT operations.

Colocation: Third-party operated facilities where multiple organizations rent space, power, and cooling for their servers.

Edge: Small, decentralized data centers located close to end-users or devices to provide low-latency computing at the “edge”.

Hyperscale: Extremely large-scale facilities (often 5,000+ servers and 10,000+ sq. ft.) designed for a single hyperscale operator.

Highlighted Projects:

Company | Location | Estimated Investment | Size/Capacity | Focus Area | Estimated Completion |

Microsoft | Mount Pleasant, WI | $1 billion | Multiple data halls | AI, cloud services | End of 2025 |

Oracle, OpenAI, SoftBank (Stargate Project) | Abilene, TX | $100 billion (total) | 10 buildings, 500,000 sq ft each | AI infrastructure | Late 2025 |

Meta | Richland Parish, LA | $10 billion | 4 million sq ft | AI, data storage | 2030 |

Amazon Web Services (AWS) | Northern Virginia | Multi-billion-dollar expansion | Multiple high-performance computing facilities | Cloud services, AI applications | Ongoing |

Lincoln, NE | $600 million | 600-acre campus | Cloud computing, AI workloads | July 2025 | |

CoreWeave | Kenilworth, NJ | $1.2 billion | 280,000 sq ft | AI, GPU cloud services | Ongoing |

Henderson, NV | $1 billion (total) | 64-acre campus | Network infrastructure, AI | Ongoing | |

Amazon | Ohio (Statewide) | $23 billion (since 2015) | Multiple facilities | Cloud computing, AI services | Ongoing |

Microsoft | New Albany, OH | $420 million | 30 MW capacity | Cloud services | Ongoing |

Meta | Davenport, IA | $800 million | 35 MW capacity | AI, data storage | Ongoing |

Cedar Rapids, IA | $576 million | 31 MW capacity | Cloud computing, AI workloads | Ongoing |

Stargate is an unprecedented gigantic, cross-company, AI-focused joint venture. Launched in early 2025, backed by OpenAI, SoftBank, Oracle, and MGX, with support from technology partners like Microsoft, NVIDIA, Arm, and more.

The initiative aims to invest up to $500 billion over four years in AI infrastructure, starting with an immediate $100 billion deployment.

Initial construction is focused on a site in Abilene, Texas, with plans for up to 20 hyperscale data centers nationwide.

The MEP Backbone of Data Centers

Water and energy are the lifeblood of modern data centers. Both are managed through the Mechanical, Electrical, and Plumbing (MEP) systems that form the backbone of every facility.

Electrical:

Servers require a constant, stable flow of electricity to run 24/7. This is an especially heavy draw when hosting compute-intensive workloads like AI, cloud applications, and big data. Since the dawn of data center builds the core site-selection process constraints were 1) Proximity to fiber network 2) Available, low cost, flat land 3) Sufficient power. Today, in the AI hyperscale era, 24/7 non-stop access to POWER is the constraint.

To prevent downtime, facilities rely on Uninterruptible Power Supply (UPS) systems, typically battery-based, with backup generators ready for extended outages. Electricians build the power distribution chain from the utility feed down to rack-level Power Distribution Units (PDUs). The scale is immense: a large data center can consume as much electricity as a small town or even a medium-sized city.

Mechanical:

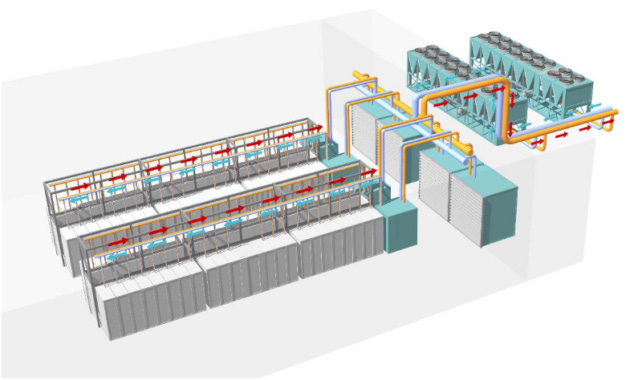

Temperature regulation for data centers is crucial as modern chips produce intense localized heat and overheating causes failures (and fires). Mechanical teams install the heating and cooling infrastructure that keeps server temperatures within safe limits. Many facilities use chilled water systems to absorb heat from servers and release it via cooling towers or other heat-exchange methods. These systems typically are made up of cooling towers, chillers, pumps, pipes, heat exchangers, condensers, and computer room air handler (CRAH) units.

The industry is increasingly switching from air-based cooling (fans, chilled air, typical HVAC systems) to liquid-based cooling (coolant flowing through pipes, cold plates, immersion baths) because air alone can no longer keep up with the heat output of today’s hardware.

Microsoft’s Closed-Loop Water Based Cooling System Per Geek Wire

Plumbing:

Data center plumbing is unique in that the plumbing infrastructure is built primarily for machines, not humans.

While most facilities still draw from municipal supplies, operators are increasingly turning to recycled, reclaimed, or non-potable water to ease pressure on local resources. Google was an early mover, using reclaimed water for its Douglas Country, GA facility back in 2012, a practice it has since expanded across multiple campuses. Amazon has committed to supplying more than 120 U.S. data centers with recycled water by 2030, part of a broader sustainability push to cut freshwater consumption. Microsoft and Meta are also pursuing similar programs, often in water-stressed regions. Microsoft’s closed loop system above won’t lose water to evaporation and has helped cut its water use down 39% since 2021.

Don’t be fooled: in hyperscale facilities, plumbing systems are more than just pipes feeding cooling towers. They’re integrated with the Building Management System (BMS) to monitor water flow, temperature, and pressure; tied to fire suppression systems engineered to protect sensitive electronics while minimizing water damage; and connected to drainage and waste lines for both routine discharge and emergencies.

Source: Google. Data center in The Dalles, Oregon releases water vapor and steam from cooling towers.

The Contractors Leading the Charge

General Contractors

Holder Construction, HITT Contracting, Turner Construction, DPR Construction, Clayco, Whiting-Turner, and Hensel Phelps have dedicated mission-critical teams and a track record of delivering large-scale data centers for both hyperscale and colocation clients.

In 2023, Holder Construction ($3.80B), HITT Contracting ($3.61B), Turner Construction ($3.36B), DPR Construction ($2.72B), and Clayco ($2.31B) each generated more than $2 billion in data center construction revenue.

MEP Contractors

On the MEP side, Comfort Systems USA and EMCOR Group stand out for their broad infrastructure capabilities and strong presence in mission-critical data center work. Southland Industries and Murphy Company are also major contributors, especially in HVAC, plumbing, and fire-protection systems. While not purely MEP specialists, firms like IES Holdings and M.C. Dean deliver critical electrical and integrated systems expertise—and often handle data center systems that bridge both mechanical and electrical domains.

Wrapping Up

The U.S. has undoubtably entered a defining moment for data center development — a sector that has quietly become one of the most powerful engines of private construction spending. From the mainframe rooms of the 1940s to today’s hyperscale campuses built for AI, each wave of innovation has demanded greater scale, reliability, and resource intensity. The modern data center is as much a feat of industrial engineering as it is of computing, with electrical, mechanical, and plumbing systems forming a mission-critical backbone that rivals the complexity of any other built environment.

If history is any guide, the next decade won’t just be about building bigger data centers, it will be about making them smarter, more efficient, and seamlessly woven into the nation’s critical infrastructure. Hyperscale campuses will serve as the digital factories of the AI age, meeting the world’s insatiable demand for computation while shaping the architecture of the global economy for decades to come.

Subscribe to CraftGild Research

Get the latest research and insights delivered to your inbox.